Mortgage Education: FHA Loans and Discount Points for First-Time Homebuyers

Understanding FHA Loans and Discount Points: A Guide for First-Time Homebuyers

Buying your first home is an exciting milestone, but it can also be overwhelming, especially when it comes to navigating the financial options available to you. If you're considering an FHA (Federal Housing Administration) loan, understanding how discount points work can be crucial in making the most of your investment. In this article, we will explore what discount points are, their pros and cons, and provide examples to help you decide if purchasing them is the right choice for you.

What Are FHA Loans?

FHA loans are popular among first-time homebuyers due to their flexible requirements and lower down payment options. They are backed by the federal government, making them less risky for lenders. Some key features of FHA loans include:

- Lower down payment: As little as 3.5% of the purchase price.

- Lower credit score requirements: Generally, you can qualify with a credit score as low as 580.

- More forgiving debt-to-income ratios: Allows for higher levels of debt compared to conventional loans.

What Are Discount Points?

Discount points are fees that a borrower can pay to lower the interest rate on their mortgage. Essentially, one point equals 1% of the loan amount. For example, if you're borrowing $200,000, one discount point would cost you $2,000. By paying these points upfront, you can reduce your monthly mortgage payment over the life of the loan.

How Do Discount Points Work?

When you purchase discount points, you are essentially prepaying interest. For every point you buy, your interest rate typically decreases by 0.25%. However, the exact rate reduction can vary based on market conditions and the lender's specific policies.

Pros of Buying Discount Points

-

Lower Monthly Payments: By reducing your interest rate, your monthly payments decrease. This can make homeownership more affordable, especially for those on a tight budget.

-

Long-Term Savings: If you plan to stay in your home for an extended period, the savings from lower monthly payments can add up significantly over the life of the loan.

-

Tax Deductions: The cost of buying discount points may be tax-deductible, which can provide additional financial benefits. Always consult a tax professional for advice specific to your situation.

Cons of Buying Discount Points

-

Upfront Costs: Paying for discount points increases your upfront closing costs. This can be a significant burden for first-time homebuyers who may already be stretching their budgets for the down payment and other closing costs.

-

Break-Even Period: The time it takes to recoup your investment in discount points can be lengthy. If you sell or refinance your home before reaching the break-even point, you may lose money.

-

Market Conditions: If interest rates drop after you purchase discount points, you may find yourself in a less favorable position.

Examples of Buying Discount Points

To help you better understand how buying discount points can impact your mortgage payments, let's walk through a couple of examples.

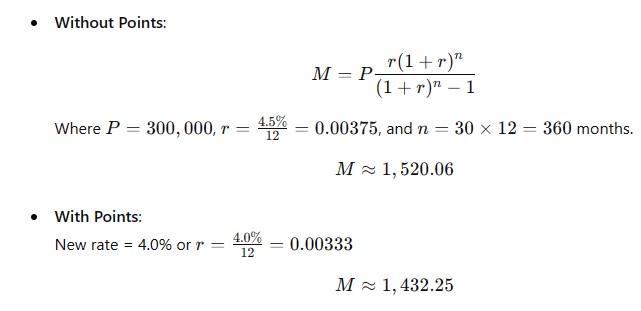

Example 1: Basic Calculation

Scenario: Sarah is purchasing a $300,000 home with an FHA loan. She has the option to buy discount points to lower her interest rate.

- Loan Amount: $300,000

- Interest Rate Without Points: 4.5%

- Interest Rate With 2 Points: 4.0%

Cost of Points:

- 2 points = 2% of $300,000 = $6,000

Monthly Payments:

Savings:

- Monthly Savings: $1,520.06 - $1,432.25 = $87.81

- Break-even Period: $6,000 / $87.81 ≈ 68 months or about 5.7 years.

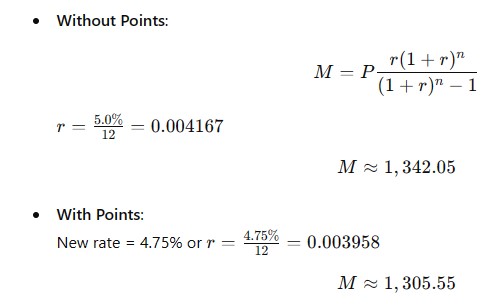

Example 2: Longer-Term Savings

Scenario: Mark is also looking to buy a home priced at $250,000 and is evaluating the same points structure.

- Loan Amount: $250,000

- Interest Rate Without Points: 5.0%

- Interest Rate With 1 Point: 4.75%

Cost of Points:

- 1 point = 1% of $250,000 = $2,500

Monthly Payments:

Savings:

- Monthly Savings: $1,342.05 - $1,305.55 = $36.50

- Break-even Period: $2,500 / $36.50 ≈ 68 months or about 5.7 years.

When to Consider Buying Points

Deciding whether to buy discount points ultimately comes down to your financial situation and how long you plan to stay in the home. Here are a few considerations:

-

How Long Will You Stay? If you plan to live in the home for more than five years, buying points might be beneficial as you will likely recoup your investment through lower payments.

-

Your Financial Situation: Can you afford the upfront cost of the points without jeopardizing your ability to cover other expenses related to homeownership? Ensure that you have adequate savings for emergencies and maintenance.

-

Interest Rate Trends: If you believe interest rates will rise in the future, locking in a lower rate now by purchasing points could be a wise decision.

In summary, purchasing a home with an FHA loan can open many doors for first-time buyers, and understanding how discount points work is an essential part of that journey. While buying discount points can lead to lower monthly payments and significant savings over time, it's crucial to evaluate your financial situation, stay duration, and market conditions before making a decision.

Remember, the best choice varies from person to person. Always consult with a mortgage professional who can provide personalized advice based on your circumstances. Whether you choose to buy discount points or not, being informed will empower you to make the best decision for your homeownership journey. Happy house hunting!